A sharper Fed takes shape under Warsh

The new chair affirmed a commitment to 2% inflation and tighter messaging

5 min read

KEY POINTS

- Warsh’s first FOMC meeting reinforced Fed independence and a firm commitment to the Fed’s 2% inflation target, easing concerns about political influence.

- With inflation still elevated and labor markets firming, the Fed held rates steady and raised expectations for fewer—or no—cuts ahead.

- Our base case is for no rate cuts this year.

Kevin Warsh, the new chair of the Federal Reserve, came in hot after leading his first Federal Open Market Committee (FOMC) meeting. If there were some worries that Chair Warsh was going to be a lackey for the president who nominated him for the position and who has been very clear and public about the direction he thinks the Fed should be taking rates, Warsh’s words and actions reduced that risk materially.

The action, or in this case inaction, taken by the Fed was no surprise. The current Fed Funds target range of 3.50-3.75% was left unchanged. Recent data on the labor market shows that it’s firming, which removes the reason the Fed had used to lower rates late last year and early this year.

At the same time, inflation data has moved further away from the Fed’s 2% target. Yes, most of this move has been led by higher energy prices which could ease based on the recent Memorandum of Understanding (MOU) between Iran and the U.S. Nevertheless, some areas of inflation outside energy are showing stubbornness at levels which remain above the Fed’s target even as other areas, like shelter costs, have been moving slowly downward. The vote to leave policy unchanged was also unanimous which reverses the recent trend of some dissents.

What was a bit of a surprise to some, was the speed at which it appears Chair Warsh wants to move as he considers the implementation of some aspects of his “regime change.” Warsh stated unequivocally that the Fed’s goal is to get inflation down. This is not to say that the Fed had changed that goal under Jay Powell, the previous chair. However, Warsh quickly squashed the idea that a new leader might have a different take on the 2% goal as opposed to something a bit more easily achieved like 3%. As an aside, The U.S. has not seen 2% inflation for over half a decade.

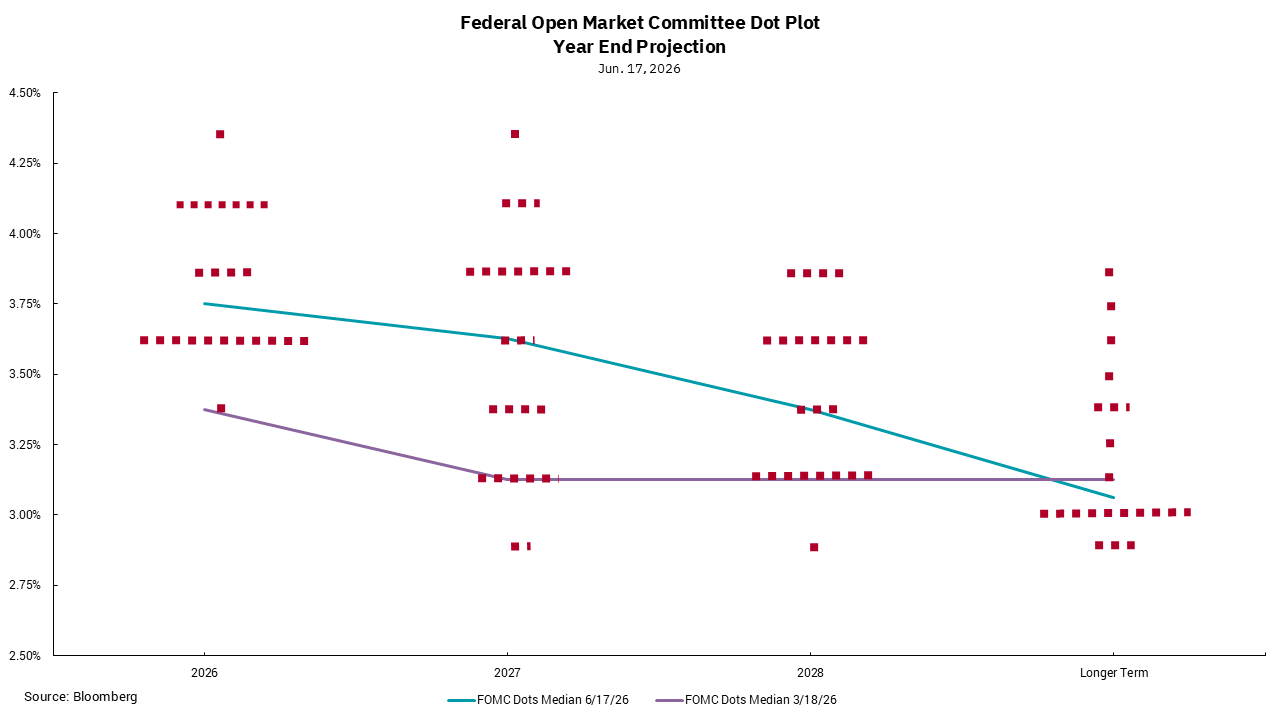

In addition, there are already some changes to how the Fed is communicating on a postmeeting basis. The post-meeting statement was shortened from an average of over 3,200 words to 130 words, while the paragraph on forward-looking guidance was removed completely. There were also changes to the “dot plot,” which is our chart this week. It is clear from the overall chart that there has been an upward shift in rate expectations since the last update. The purple line in our chart shows the central tendency of the previous dot plot versus the blue line, which is the current central tendency. Instead of two rate cuts in 2026 we now see zero rate cuts, and there are significantly more Fed members who now see rate increases over the course of the next year. In another change, Chair Warsh noted that he did not put his dot on the chart, so there are only 18 dots instead of 19.

There was also an announcement of some new task forces set up to review aspects of the Fed and its monetary policy framework. These task forces will be reviewing topics like the balance sheet, communication, their data sources, productivity and jobs (a nod to the potential impacts of artificial intelligence [AI]) and the inflation-measuring framework. When I hear about things like this, I am reminded of a lesson I have learned in business over the years: never confuse a meeting with progress. In this case, never confuse a task force with action. However, it would seem the capital markets need to prepare for a different Fed going forward than what we have had. We will be discussing the implications of these changes in future missives but, for the time being, we think the bar for lowering rates is higher than the bar for rate increases. No action is still our base case for 2026.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)